When Samsung started producing AMOLED displays in 2007, AMOLED technology was at a very early stage, immature, and Samsung took a huge risk. A few years later, this risk was rewarded with a successful display business and a boost to the company's smartphone business that was the first to adopt AMOLED displays.

Fast forward to 2016, and today Samsung is still the king of AMOLED displays, with a market share of over 95% in small/medium AMOLED panels. If we look at OLED TV production, then LG Display is the only commercial producer at this stage. But Samsung and LG are not alone - several companies in China and Taiwan already started mass producing AMOLEDs, and others have announced plans for large AMOLED fabs. In this long article we'll list all of these AMOLED producers and developers (over a dozen) - and details their current production capacity and rumored and confirmed production plans.

So we will start indeed with Samsung Display - which is the largest producer by far, but also the company that almost does not communicate any production capacity numbers and plans. Samsung's current capacity is about 300 million AMOLED display in a year, out of which almost 100 million are flexible displays - produced at the company's A3 Gen-6 Flexible OLED line that can handle around 15,000 substrates per month.

SDC's AMOLED supply is quite tight - and the company is refusing new orders from companies. According to report SDC plans to double its AMOLED capacity by around 2019. The company reportedly signed a contract to supply 100 million flexible AMOLED panels to Apple starting in 2017 or 2018.

According to a report earlier this year, SDC decided to double the capacity of its A3 flexible OLED line. $325 million in new equipment orders were already placed which will increase A3's capacity to 30,000 monthly substrates by early 2017. According to a different report Samsung Display will invest around $6.8 billion in 2016 to boost capacity, which will translate to a yearly capacity of over 200 million smartphone-sized panels.

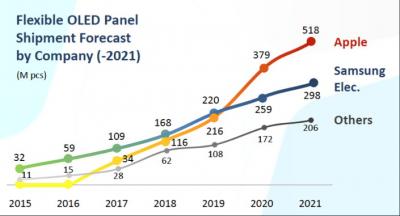

Some analysts such as UBI estimate that there will be over 500 million flexible AMOLEDs produced in 2019 and over a billion such panels in 2021. Most of this production will be made by Samsung Display. You can see UBI's flexible OLED shipments forecast by customer (not by producer) above. In the chart below you can see the OLED Association's forecasts for flexible OLED production (by producer, this time).

The second largest AMOLED maker is LG Display. The company is currently focused on large-area OLED TV panel production, but it is quickly moving into small/medium flexible OLED production (having admitted that it was late to this market). In 2015, LGD shipped around 400,000 OLED TV panels and the company's goal is to produce 1 million such panels in 2016 and over 1.5 million in 2017.

LGD is currently producing OLED TVs in the M2 fab in Paju, that has a capacity of 34,000 monthly Gen-8 substrates (together with the smaller pilot line that is also operative). LG Display also has a smaller Gen-4.5 fab used to produce plastic-based OLEDs - with a monthly capacity of 14,000 substrates (mostly used for wearables - including Apple's Watch).

LG announced and started constructing several AMOLED fab. First up is the E5 line, a 6-Gen (1500x1850 mm) flexible OLED fab that is estimated at $900 million. The new E5 line will have a capacity of 7,500 monthly substrates - or 1.5 million 5.5" panels, and will begin operation in the first half of 2017. LG already started to install equipment in that fab.

In addition to the E5 line, LG already announced plans to build the E6 line - a new 6-Gen (1500x1850 mm) flexible OLED production line in Paju. The investment in the new E6 line will total $1.7 billion USD and it will have a monthly capacity of 15,000 G6 substrates, and is scheduled to begin production in the second half of 2018.

In August 2015 LG Display announced plans to invest around $8.5 billion in OLED capacity in the next three years as the company shifts its focus to OLED displays. Later in November LGD announced that it will build a new OLED display plant in Paju, Korea - the P10 fab will mainly make large-size OLED TV panels, but it will also produce flexible OLED panels. The total investment in the P10 plant is estimated at KRW10 trillion ($8.7 billion USD).

In early 2016, LG Display said that it will invest a further $380 million to expand its OLED TV production capacity. LGD will convert an existing LCD production line to OLED production. The investment will begin in Q1 2016 and will be completed by Q2 2017.

Moving from Korea to Japan, there are two AMOLED developers that are progressing towards mass production. Even though Sharp was quite against OLEDs up until a few years ago, following the acquisition by Foxconn Sharp is moving fast towards AMOLED mass production, especially since the Japanese display maker is set to become an Apple supplier.

Foxconn allocated to Sharp around $1.8 billion towards OLED development and production, with initial plans to start production in 2017. This was too optimistic, and if Sharp could mass produce AMOLEDs in 2018 it will be considered a success. In October 2016 Sharp announced that it will invest $570 million in its OLED business. The company will establish pilot lines at its plants in Osaka and in the Mie Prefecture, and those lines will begin OLED production in the summer of 2018. These are pilot lines, but Sharp does aim to produce commercial panels at these initial fabs.

Japan's second OLED developer is Japan Display (JDI). JDI was formed in November 2011 by Sony, Hitachi, and Toshiba who combined their small/medium panel production capabilities and received $2 billion from Japan's Innovation Network Corp (INCJ). The company is supplying LCD panels to Apple.

JDI has been developing OLEDs since its inception, and the company does have plans to start mass producing OLED panels as it aims to remain an Apple supplier. JDI has plans to produce AMOLED display by 2018, but no definite investments have been announced yet.

Interestingly, Sharp expressed wishes to collaborate with JDI as the two companies are quite behind the Korean and Chinese OLED makers. It is too early to know if the two Japanese companies will actually join hands in their OLED efforts.

Now let's consider Taiwan. First up we have AU Optronics, who's been developing AMOLED technologies for ages. AUO is producing AMOLED displays commercially at its AFPD Gen-4.5 LTPS fab in Singapore. Production capacity is quite limited, and the company is focused on OLED displays for the wearable market, and VR AMOLEDs.

AUO has not yet detailed any plans to initiate real AMOLED mass production. Towards the end of 2016 the company will start producing LTPS LCDs in a new Gen-6 line in China, and according to report it may convert some of that capacity to AMOLED production in the future.

Taiwan is also home to Innolux, a display maker that is a subsidiary of Foxconn. Innolux has been demonstrating OLEDs for a long time, but has not yet started production. In 2016 Innolux demonstrated new rigid and flexible AMOLED prototypes, and the company said it aims to mass produce AMOLEDs - starting in 2017 with small-sized displays for wearable applications.

The company's CEO is still skeptical on the competitiveness of OLEDs, so it is not clear whether this promise to produce AMOLEDs will result in actual production. Following Foxconn's Sharp acquisition it's plausible that Innolux and Sharp will integrate their OLED efforts - so it is hard to predict how will AMOLED production at Innolux will take shape.

The third OLED developer in Taiwan is Chunghwa Picture Tubes (CPT). CPT has an existing pilot 4.5-Gen AMOLED fab - used to produce AMOLEDs in very small volume. In recent years CPT has been collaborating with ITRI and FlexEnable to developer flexible AMOLED technologies, and has stated that it will initiate flexible OLED production in 2017.

Some speculate that CPT will use ITRI's technology and also integrate ITRI's existing 2.5-Gen flexible AMOLED production line into its own fab. ITRI is also looking into IGZO and OTFT technologies. CPT is building a new 6-Gen fab in China, with an investment of about $1.85 billion - and some reports suggest that CPT plans to produce IGZO backplane OLED panels in the second phase of this fab.

Finally, we move to China. There are several Chinese display makers, and most of these companies are developing OLED technologies - and indeed diverting investment from LCD to OLED capacity.

We'll start with Everdisplay (EDO). Everdisplay started mass producing 5" 720p AMOLED displays towards the end of 2014 in a 4.5-Gen line with a monthly capacity of 20,000 substrates. Since then the company added more displays - wearable panels and larger 5.5" ones. Everdisplay is also developing flexible panels, transparent panels and high-density AMOLEDs for VR applications. According to reports, Xiaomi's Redmi Pro smartphone uses EDO's (and BOE's) 5.5" FHD AMOLED panels.

According to a report a few months ago, Everdisplay is planning to invest $4.1 billion USD to build a 6-Gen AMOLED factory. The upcoming factory will have a monthly capacity of 30,000 substrates and will start trial production in 2018. Mass production in the new fab is expected by early 2019 - and will include panels from 1 to 13 inches.

BOE Display (the second reported supplier to Xiaomi's Redmi Pro) is producing AMOLED displays at its 5.5-Gen LTPS OLED fab in Ordos - although capacity is still limited as the company struggles with low yields. BOE Display is building a second AMOLED fab, a Gen-6 OLED (LTPS) fab in Chengdu. The company started working on the new fab in May 2015, and said that the total investment will reach around $3.54 billion. This fab will have a capacity of 45,000 monthly substrates - and is expected to begin mass production in 2017.

In October 2016 BOE signed a framework agreement with the Miangyang government in Sichaun to establish a second Gen-6 (1500 Ã 1850 mm) flexible AMOLED fab. Total investment in this fab is estimated at 46.5 billion yuan ($6.87 billion USD) and capacity will be 48,000 substrates per month. BOE aims to start construction in the second quarter of 2017 and mass production will begin in 2019.

BOE is also looking into a Gen-8 OLED TV fab, which it has a plan to build in Hefei. This fab will cost around $1 billion, but it seems the decision has not been made yet - although the company did already receive a $20 million grant from the local government. Using an existing pilot line, BOE produced 55" 4K OLED TV samples as early as 2014.

China's Visionox has started mass producing AMOLED panels in June 2015, but the company's production capacity is still limited. Visionox's Gen-5.5 AMOLED line in Kunshan can currently produce around 4,000 monthly substrate, and once yields stabilize they will reach a full capacity of 15,000 monthly substrates. The company is mulling a $673 million investment to expand the capacity of this fab.

According to a report earlier this year, Visionox is aiming to establish a 6-Gen flexible AMOLED fab in Chengdu. Work will begin towards the end of 2016. This hasn't been confirmed yet.

Shanghai-based TianMa is starting to produce glass-based OLEDs in its Gen-5.5 pilot line - but this line will have a limited capacity. Commercial production is expected by the end of the year. TianMa did not yet reveal any investment plans for AMOLED mass production, but the company did establish a joint venture called Johua Printing with CSoT to promote printed OLED technologies.

Back in 2013 TianMa announced plans for three different AMOLED production fabs, but it's not clear if any of this is still on track, except the existing Gen-5.5 pilot line mentioned above.

TCL's subsidiary CSoT is indeed moving forward with OLED production. The company announced an ambitious plan to construct a $6.96 billion LCD and OLED Gen-11 production fab in Shenzhen. The new fab, built by TCL and Shenzhen Huaxing Power with help from the Shenzhen Economic and Trade Commission, will have a monthly capacity of 90,000 Gen-11 substrates (3370x2940 mm) and use IGZO backplanes.

CSoT announced plans to increase investment by a further $3.15 billion, and Samsung will hold a 9.76% stake in this new fab. CSoT aims to start building the fab towards the end of 2016, and construction is planned to end by January 2018 and equipment will begin installation in July 2018. Mass production will begin in April 2019. The fab will produce a wide range of LCD TVs (43 to 75 inch) - and OLED TV panels, using "printing OLEDs" technologies.

CSoT is also building a Gen-6 LTPS line in Wuhan, China, in a $2.6 billion investment. Reports suggest that the company is actually ahead of schedule, and estimates that mass production will begin in Q1 2017. The plan is to make both small and medium sized displays - LCDs and OLEDs. The new production line will have a capacity of 30,000 monthly substrates - it's not clear what will be the ratio between high-end LCDs and OLEDs.

The final company discussed in this report is Truly Semiconductors. The Hong-Kong based OLED producer is one of the world's leading PMOLED maker, and in 2014 the company announced its entry into AMOLED production.

Truly is building a 4.5-Gen AMOLED fab that will have a monthly capacity of 15,000 substrates. The company can expand this to 30,000 with a further investment. Production is set to start any day now, although it may take a while to actually commence shipping commercial panels.

Truly never demonstrated any flexible OLEDs, nor announced any plans to produce such panels - but a report from Korea suggests that Truly does aim to start producing flexible OLEDs in the near future.

Comments

Yes, this article lists factory plans in addition to cost and capacity. Of course in many times factories take longer to start-up than planned...

Does this let us know when factorys come online?