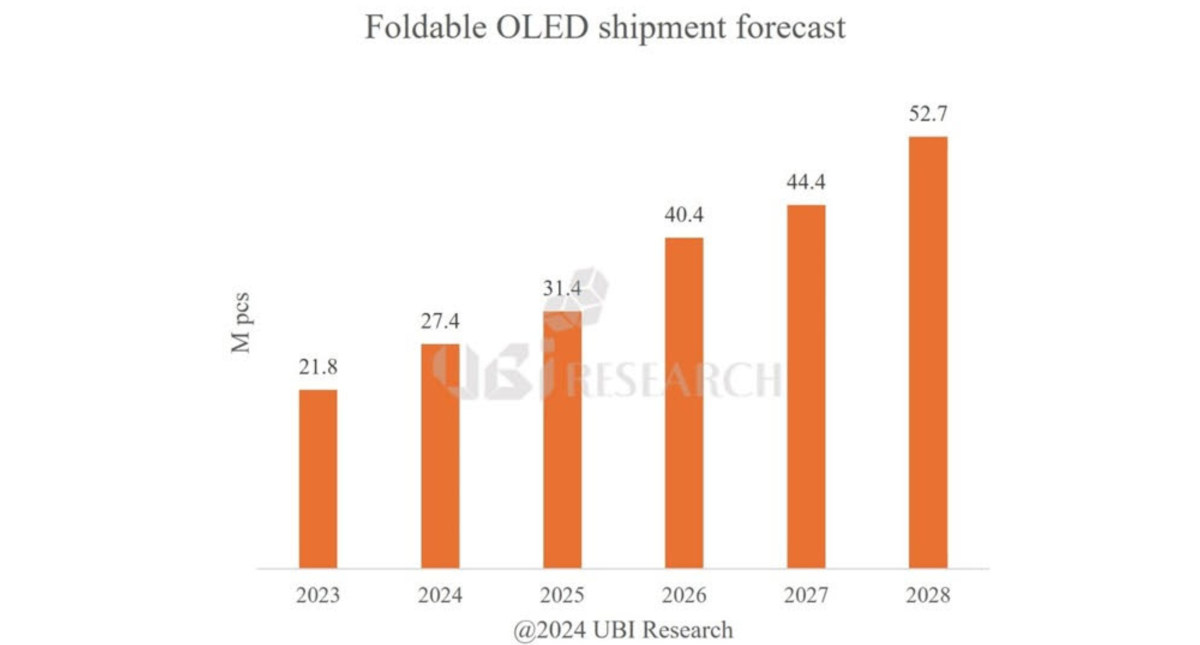

UBI: the foldable OLED market will grow to 52.7 million units in 2028, Samsung Display to remain the market leader

UBI Research released its latest foldable OLED shipments forecast, saying that it expects the market to grow from 27.4 million units in 2024 to 52.7 million 2028.

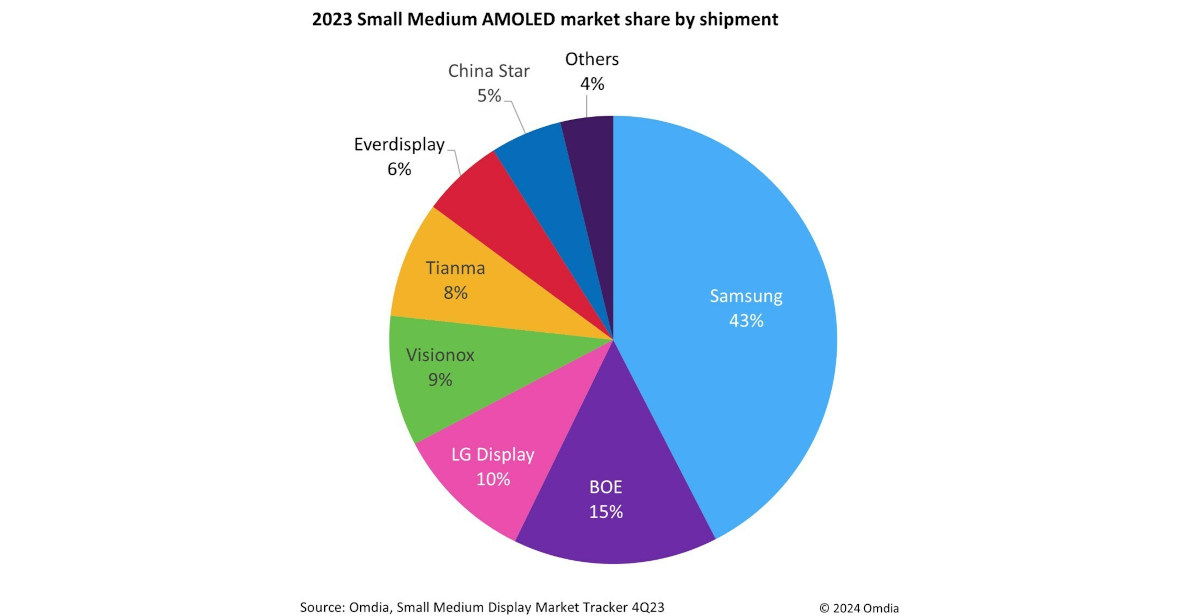

The market is dominated by Samsung Display, which shipped 13.4 million foldable OLEDs in 2023, and holds a 61% market. Samsung is followed by BOE (6.2 million, growing 3X from 2022), TCL CSOT (1.1 million) and Visionox (1.1 million). UBI expects Samsung Display to remain the clear leader in this market as it is the sole supplier to Samsung Electronics - and it is also expected that Samsung will be the exclusive supplier to Apple's future foldable iPhones.

Read the full story

Posted: Apr 03,2024

")