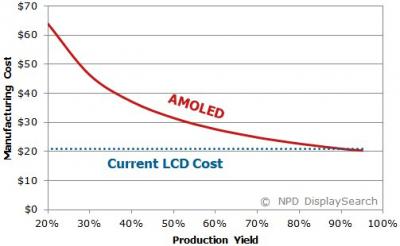

DisplaySearch says that manufacturing costs for small-sized AMOLEDs are currently about 10-20% higher than comparable LCDs. A 5" Full-HD AMOLED for example, costs 16% more than a comparable LCD one.

But improvement in production yields will lower the gap - and in fact DisplaySearch sees OLEDs becoming cheaper than LCDs within two years, when AMOLED production yields reach 90%. DisplaySearch also says sees OLED materials cost reductions, which will also reduce prices further.

It was always assumed that OLEDs could be made cheaper than LCDs as they do not require a backlight and they have fewer components (light diffusers, color filters, etc.). But the more difficult production methods kept AMOLED prices high.

Some estimate that next-generation production methods (for example ink-jet printing) will enable even cheaper AMOLED production.

Comments

Interesting analysis Rob.

Just to set things straight: out of the $146.6 million in 2013 revenue, $40 million are the SDC license (easy). But the rest is not only Samsung. My own estimate is that SDC paid $85 million for materials. So it's about $125 from SDC, or about $1.2 per screen. Very rough estimates, as you said yourself.

...either too high or too low...but these rough calculations show the magnitude of the cost of the panel vs the cost of the emitters/host (at least those sold by UDC). I guess it doesn't count the flourescent blue and host that is in the panel, nor the red host...but again, the numbers don't change dramatically.

It also gives one comfort that eventually the cost of OLED lighting can come down dramatically, after all, lighting is a much simpler product to produce. Having said that, the grams of materials needed per meter2 might be fairly similar for UDC to sell. And since "lifetime" is an even more important variable for lighting (vs a smartphone), it is even more important for the highest quality "ingredients" (including host) be used.

The LCD may be less costlier than the AMOLED in raw cost per unit. But if you factor in the LCD backlight (CF or OLED) and the additional high voltage electronics to power the LCD, the results are obvious that a new smartphone with an AMOLED is less costlir to manufacturer than one with a LCD.

Judging by the analysis here for OLED on a discussion RE: AMOLED technology costs, the same can be said. I'm excited for OLEDs prospects in the coming years and hope to see many cool applications of the tech.

LONG: OLED

R2R manufactoring method costs will reduce costs even further for Amoleds

made with InkJet technology.When this manufactoring method will be introduced for Amoled displays?

And the progress towards Woled,Roled,Yoled where Woled=White oled will be very common within 5-years as light source in ceilings and Roled=Red oled and Yoled=Yellow oled as two other types of monochrome oleds will be very common

as rear lights in cars and other vehicles and both Roled and Yoled in superthin

traffic signs.

So,progress towards R2R manufactoring of Amoleds will benefits of more displays

than only for electronic gadgets like smartphones,smart watches and pc and for TV.

When Ron wrote up his 20X optimistic piece for Seeking Alpha he based his projections off of Samsung's 2013 actual production of 5" panels. What jumped out at me in its simplicity is that in 2013 SMD produced about 150 million 5" panels and Universal Display (UDC) received about $150 million in revenue from Samsung ($146.6 million to be exact, but close enough for rounding). In other words, UDC received about $1 for every panel produced. Now of course this revenue includes materials that SMD used in other areas (pilot TV production etc.) and it also includes material that was "lost" due to yield issues. On the flip side, it does NOT include full production using any of the new emitter materials SMD used in Q1 of '14 nor does it include a full year of green host sales. So with all of the caveats of a "rough" number, it is still interesting to think about the fact that UDC "only" received $1 per screen.

So if we believe in the accuracy of the DisplaySearch numbers cited in this article, the $1 per screen of cost that UDC receives is still a pretty small fraction of the total cost of the screen. The reality of the cost is such that if yield is 70% then effectively 30% of the materials that UDC is selling is being wasted, so if yield goes up, the revenue per screen actually produced will go down, but that cost will not go down due to the price SMD is paying rather it will go down due to yield improvments.

So if the delivered cost of an AMOLED panel is more YIELD related than MATERIALS related, it seems to me that UDC is now, and will continue to be in the drivers seat. For example, if total UDC sales per screen is $1, the percentage of HOST is perhaps 25% of that. But if the correct host will help drive the yield down, will SMD switch host to save a few pennies per screen, if that switch runs the risk of decreasing yield?

DisplaySearch predicts that the cost of materials will also drop. I have no doubt that if UDC charges $150 million for X grams of materials and a producer wants to buy 6.66X of materials, then UDC will "discount" that price below $1 billion, but given that a producer has no other avenue for product, due to both patent protection (emitters) and quality (host) the discount that UDC needs to provide will be modest.