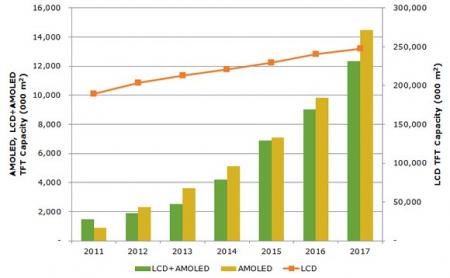

DisplaySearch says that OLED TV panels production costs are still very high, but this will not deter investments and the company forecasts rapid expansion in AMOLED capacity, as can be seen in the chart below (in which the yellow bars show AMOLED capacity while the green bar is capacity that can be used for either LCD or AMOLED production):

According to this chart dedicated AMOLED fab capacity grew from less than a million square meters in 2011 to almost four million square meters in 2013. In 2017, dedicated AMOLED capacity will reach 14 million square meters (i.e. 28 times as much capacity as in 2011).

DisplaySearch says that a 55" LCD TV costs about $426 to make. A similar RGB (direct emission) OLED TV will cost $7,300 while a WRGB OLED TV will cost about half ($3,600). Interestingly, Samsung's RGB OLED TVs are currently cheaper than LG's WRGB ones. Perhaps this is just due to the fact that Samsung is being very aggressive.

A few months ago DisplaySearch estimated the total manufacturing cost of a 55" FHD AMOLED panel at $2,454. I think those new, higher, numbers make more sense if we consider the fact that the cheapest 55" OLED TV costs $9000 (Samsung's KN55S9C in Korea).

DisplaySearch says the main reason for the high OLED production costs are low yields, investment in expensive manufacturing equipment and high OLED material costs.

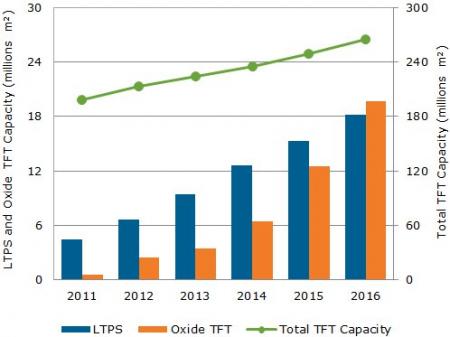

DisplaySearch further forecasts that high-performance LTPS and Oxide TFT backplanes are expected to grow very rapidly. Oxide-TFT ramp-up is about two years behind what analysts expected and there are still manufacturing challenges. Currently Sharp is the only Oxide-TFT LCD maker and LGD is the only Oxide-TFT AMOLED maker. But still Oxide-TFT is expected to grow quickly - faster than LTPS in coming years.

As you can see from the chart above, LTPS production capacity will double from almost 9 million square meters in 2013 to 18 million square meters in 2016. Oxide-TFT will grow from 3.5 million square meters to over 19 million square meters - exceeding LTPS by 2016.